At tax time we like to see receipts for vehicles, large assets, or items financed through a loan for your business or farm.

We rarely request any other receipts; for the sake of time and efficiency we generally focus on your summarized numbers. But we feel it is important for you to know how to substantiate your business write-offs in the case of an IRS audit.

Mileage

This issue has been taken to Tax Court many times and the IRS has been successful in disallowing travel deductions which do not have complete and proper substantiation. The IRS requires taxpayers to retain specific documentation to substantiate the business use of a personal vehicle under Code Section 274(d)(4). A deduction is not allowed unless the taxpayer properly documents:

- The amount of the expense (the number of miles driven)

- The time and place of travel

- The business purpose of the travel

We have also found odometer readings which correspond to the mileage listed on oil change invoices to be helpful in providing substantiation support.

Business and Farm Deductions

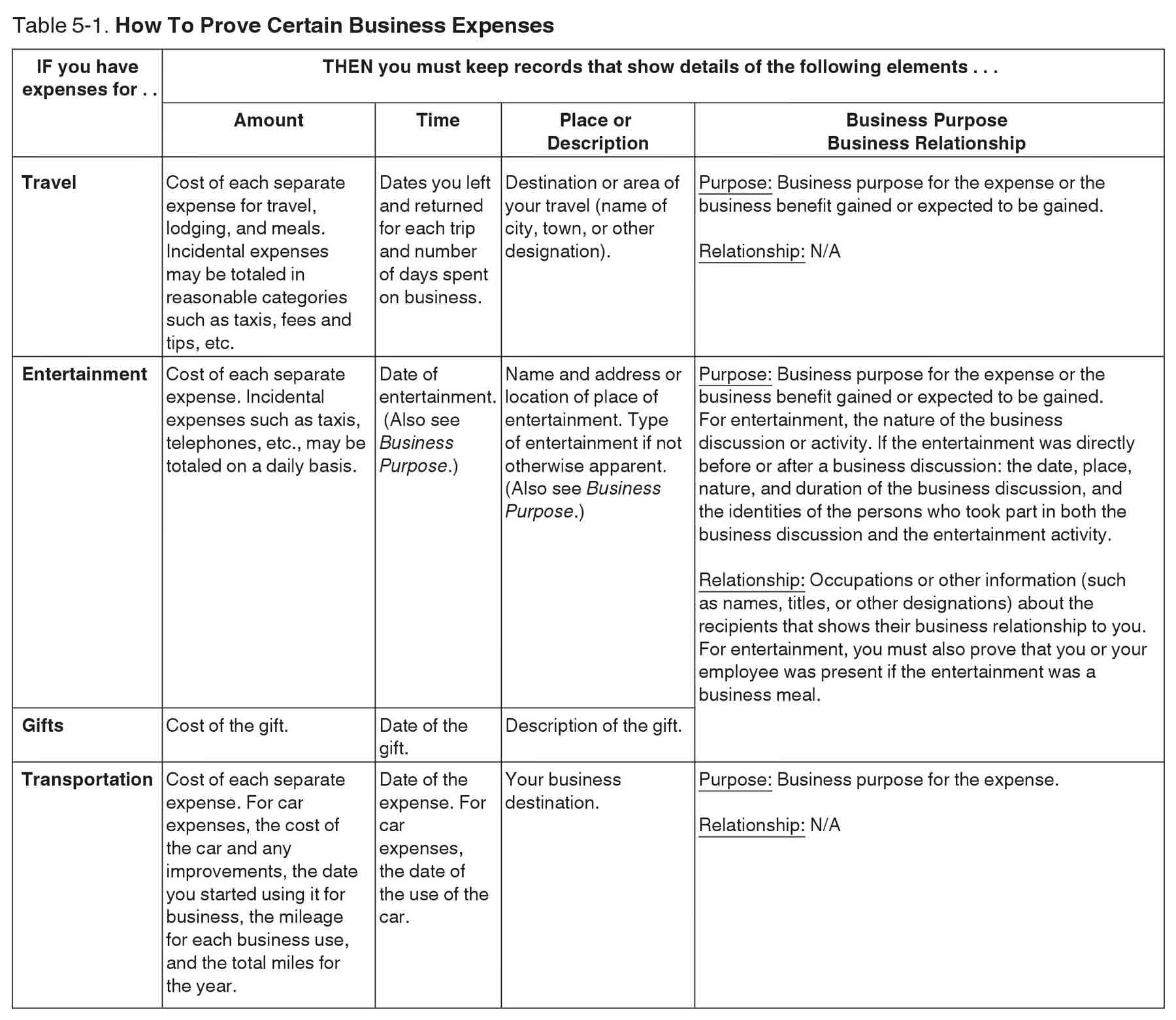

The chart below, from IRS Publication 463, describes how to prove certain business expenses by category:

In addition to travel, meal, and entertainment expenses, there are other expenses you can deduct including advertising, dues, training costs, internet, phone, legal and professional fees, tax preparation fees, supplies, rent, interest, taxes, licenses, utilities and more. You must be able to document the amount, time, place, and business purpose of each of these items in order to prove the deduction. So remember to save those receipts!

For more information see Publication 535 or contact your professional advisor.